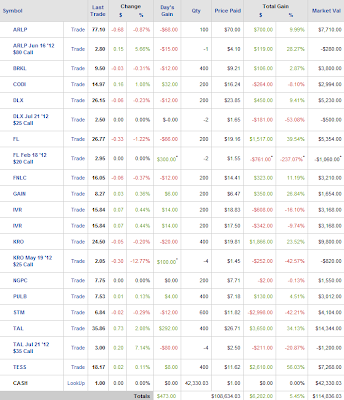

A Macro View: Stock Picking based on PPI Index

The recent release of the PPI index and core PPI has sparked some interest in how it is related to stock market returns. Calafia Beach Pundit thinks that the

PPI inflation Of 3.5% points to higher yields ahead.

From my regression research, the PPI index has the highest correlation with stock market returns by sector versus the CPI indexes of core and headline. Results for back-testing over the last 10 years also resulted in greater returns for the PPI over the CPI although core CPI does better than the headline CPI. But for the PPI versus core PPI, the results for the core PPI are very weak and much lower than the S&P 1500 flat weighted. Even when adding core to the headline PPI results in lower returns than just PPI.

The above regression analysis was in regards to sectors and stocks that performed well when the index was going up, that is, inflation heating up on the consumer side or the producer side also called "Lovers". This week's stock picking is based on a regression back test from July 2000 until the latest release in February for January's numbers. It performed better than the S&P 1500 flat weighted and achieved nearly 10% annualized return over the back test period. The following stock picking list is the "Lovers" list and filtered by Sabrient's Strong Buys and Buys.

Assurant, Inc.,AIZ, STRONGBUY

Peabody Energy Corporation,BTU, STRONGBUY

Nabors Industries Ltd.,NBR, STRONGBUY

Baker Hughes Incorporated,BHI, BUY

BB&T Corporation,BBT, BUY

ConocoPhillips,COP, BUY

CSX Corporation,CSX, BUY

Halliburton Company,HAL, BUY

Helmerich & Payne,HP, BUY

International Paper Company,IP, BUY

PerkinElmer,PKI, BUY

Pioneer Natural Resources Company ,PXD, BUY

SunTrust Banks,STI, BUY

Zimmer Holdings,ZMH,BUY

CARPE DIEM: U.S. Manufacturing Is Open for Business and Doing Well; Despite, Not Because of, Government Policy

CARPE DIEM: Chart of the Day: Drill, Drill, Drill = Jobs, Jobs, Jobs

Lovers:

Symbol Rating Price * Market Cap SABRIENT SCORES

Value Growth Momentum

AIZ STRONGBUY 43.97 Mid-Cap 88 33 63

BTU STRONGBUY 35.96 Large-Cap 97 65 15

NBR STRONGBUY 19.16 Large-Cap 98 86 41

BHI BUY 47.9 Large-Cap 98 83 32

BBT BUY 29.65 Large-Cap 62 59 97

COP BUY 72.81 Large-Cap 74 49 24

CSX BUY 21.94 Large-Cap 92 78 43

HAL BUY 36.14 Large-Cap 98 90 32

HP BUY 59.31 Large-Cap 78 95 53

IP BUY 33.02 Large-Cap 70 38 93

PKI BUY 26.07 Mid-Cap 44 94 78

PXD BUY 111.85 Large-Cap 18 87 71

STI BUY 22.28 Large-Cap 96 33 87

ZMH BUY 61.25 Large-Cap 54 72 70

PPI inflation Of 3.5% points to higher yields ahead.

From my regression research, the PPI index has the highest correlation with stock market returns by sector versus the CPI indexes of core and headline. Results for back-testing over the last 10 years also resulted in greater returns for the PPI over the CPI although core CPI does better than the headline CPI. But for the PPI versus core PPI, the results for the core PPI are very weak and much lower than the S&P 1500 flat weighted. Even when adding core to the headline PPI results in lower returns than just PPI.

The above regression analysis was in regards to sectors and stocks that performed well when the index was going up, that is, inflation heating up on the consumer side or the producer side also called "Lovers". This week's stock picking is based on a regression back test from July 2000 until the latest release in February for January's numbers. It performed better than the S&P 1500 flat weighted and achieved nearly 10% annualized return over the back test period. The following stock picking list is the "Lovers" list and filtered by Sabrient's Strong Buys and Buys.

Assurant, Inc.,AIZ, STRONGBUY

Peabody Energy Corporation,BTU, STRONGBUY

Nabors Industries Ltd.,NBR, STRONGBUY

Baker Hughes Incorporated,BHI, BUY

BB&T Corporation,BBT, BUY

ConocoPhillips,COP, BUY

CSX Corporation,CSX, BUY

Halliburton Company,HAL, BUY

Helmerich & Payne,HP, BUY

International Paper Company,IP, BUY

PerkinElmer,PKI, BUY

Pioneer Natural Resources Company ,PXD, BUY

SunTrust Banks,STI, BUY

Zimmer Holdings,ZMH,BUY

CARPE DIEM: U.S. Manufacturing Is Open for Business and Doing Well; Despite, Not Because of, Government Policy

CARPE DIEM: Chart of the Day: Drill, Drill, Drill = Jobs, Jobs, Jobs

Lovers:

Symbol Rating Price * Market Cap SABRIENT SCORES

Value Growth Momentum

AIZ STRONGBUY 43.97 Mid-Cap 88 33 63

BTU STRONGBUY 35.96 Large-Cap 97 65 15

NBR STRONGBUY 19.16 Large-Cap 98 86 41

BHI BUY 47.9 Large-Cap 98 83 32

BBT BUY 29.65 Large-Cap 62 59 97

COP BUY 72.81 Large-Cap 74 49 24

CSX BUY 21.94 Large-Cap 92 78 43

HAL BUY 36.14 Large-Cap 98 90 32

HP BUY 59.31 Large-Cap 78 95 53

IP BUY 33.02 Large-Cap 70 38 93

PKI BUY 26.07 Mid-Cap 44 94 78

PXD BUY 111.85 Large-Cap 18 87 71

STI BUY 22.28 Large-Cap 96 33 87

ZMH BUY 61.25 Large-Cap 54 72 70

Labels: Equity Markets, Macro-Economics

posted by Ronald Rutherford at 9:02 PM

1 comments

![]()

![]()