This year has brought forth the meme that public sector employees are paid more than their counter-parts in the private sector. Certainly the center of this debate has concentrated on Wisconsin and of course the Governor Scott Walker. The Economist sums up some of the points at

Wisconsin public unions: Don't join the government to get rich. The most obvious point is that some career choices have monetary consequences, and clearly top corporate lawyers can make a ton of money and vastly beyond district attorneys. But I think most people consider a lot of the non-monetary aspects of jobs also when deciding which career to pursue, like working environment, job security, stress levels, safety, job turnover, and of course under the constraints of the individual's innate abilities and interests.

The Economist links to a study by Jeff Keefe at the Economic Policy Institue which has been at the forefront of defending public sector employees as not being overpaid. In these types of studies, instead of comparing similar jobs, they compare workers across education levels, experience, hours of work, organizational size, gender, race, ethnicity and disability. Aside from education levels, the rest of the factors are not mentioned as being significant.

This raises two issues with education levels of public employees. First, as the studies themselves point to there is not equality in job titles/responsibilities. Thus the pay scales for education majors in like music, history, English, etc is indeterminate but not likely to be at the same level as public employees. Second, there are various reasons to believe that the government relies more heavily on education as requirements for a job than the private sector would. In the desire to be non-discriminatory, it is easier to use education credentials during recruitment to weed out the possible candidates to a reasonable pool than it is to use more subjective requirements and tests.

If in fact people are over-educated for the jobs they receive through the government, then this is not simply a matter of government budgets paying for those unneeded levels of education but also a dead-weight loss to society. Instead of resources {human resources} going to the most productive sectors of the economy, they get diverted to bureaucracy. For example, foreign aid often diverts skilled, educated labor into administering aid instead of the creation of an entrepreneurial class.

The Economist magazine goes on to make another important point that government employees feel entitled to the pensions plans that the unions and government agreed to and reneging on that is grossly unfair. Truly we should feel sympathetic to their plight, but there are questions that the bargaining is not between two diametrically opposed interests. A good way to describe this relationship is from Mark Perry at Carpe Diem who quotes Katherine Kersten (

The Vicious Cycle of Government Unions).

Here's the vicious cycle: Union leaders take money from union dues and pass it to Democratic candidates. Once elected, the politicians "negotiate" with the unions that helped elect them. In essence, the unions hire their own bosses who face them across the bargaining table.

Politicians repay unions' financial support by doling out hefty pensions and benefits. It's easy to be generous when you're spending taxpayers' money, not your own. Elected officials aren't accountable to a board of directors or shareholders, and they don't have to worry about going bankrupt, as private companies do.

Not that private firms don't do it, but clearly there is a tendency to push benefits into the future. Most of the reports seem to overlook what the discount rate is for calculating net present value of future benefits. It seems conceivable that public employees might have a lower discount rate than the general population. This would mean that future payments have more value than present, and that government should use that lower rate to calculate present benefits. That would then lead to lower benefits currently.

Paul Krugman also sides with the unions, surprise, surprise, surprise. At his post

The Contribution Scam, he quotes David Cay Johnston. They both feel that pensions and the benefits package come out of the workers "pay" as that was negotiated in the contracts, and supposedly the government workers would earn more than they could have if benefits were lower. The difference is whether public employees are judged by their productivity to society. In a private firm, yes there can be overpaid employees, but unlike in the fairy tales of Dilbert, competition pushes inefficient producers out. What mechanism will push government to use its resources (human capital) in the most efficient manner?

The Economist article ends with a discussion about unions being a form of monopoly market power and questions then why don't they earn even more than their counter-parts in private institutions. From the discussion above and some data below, there is in fact some questions as to whether the public employees are being taken advantage of. One reason the Economist gives is that government is a "monopoly employer" especially concerning specialized jobs that do not have equals in the private sectors. This may be just a blog post at the Economist, but the correct term is that the government is a monopsonist employer. A monopsonist is a market participant that is the sole or nearly the sole buyer of a product or service. Government being in that position, it could extract higher levels of productivity and thus create more social good, but that has not happened. Inefficiencies in government have persisted. When a monopolist sells to a monopsonist, then who captures the rents is indeterminate and falls mostly to the one that that can capture political influence.

So What is the Elephant in the Room?Other than entrepreneurs and risk takers in society, most middle class people desire to work in government. This is mostly anecdotal experiences for myself, but nothing seems to counter that for the average worker they deeply desire to work for the government. The task of social scientists like economists is to determine why. One of the best ways to determine what people want most, is to see how they "vote with their feet". This does not tell us the benefits from moving to a new location like the US or another state or just a new job, but it does tell us that the benefits exceed the opportunity costs from staying at present location.

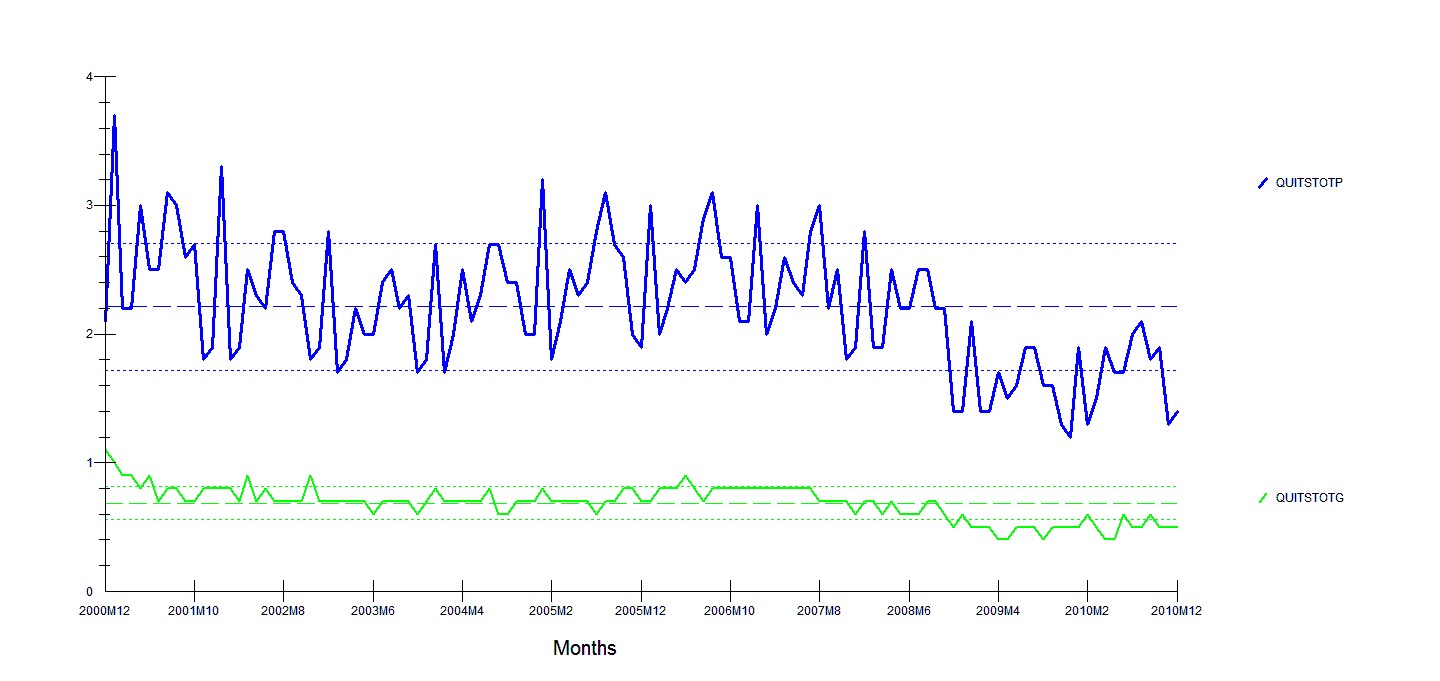

So what data points might tell us how people are voting with their feet? Job openings do not tell us how the prospective employee is reacting in the market, but quits and separations tell us the rate of them leaving the job. Ideally, we would also want to see number of applicants per job announcement or some other number to show the desire of prospective employees to be hired. The graph below is the rate of total separations for private and government employees, and the second is the rate of quits for both sectors. Both are from the Federal Reserve Bank of St. Louis over the last ten years.

Just for comparisons, I also include the two sets of data with the origin at zero and include the mean and one standard deviation for all four series.

Some things to note on the graphs are: since the last recession started separations and quits have been declining for both private and public employees as more are staying on the job longer; total separations for government employees spiked up because of the census workers laid off but still maintained its below average rate; volatility as measured by standard deviation is much greater for private employees and most dramatic for quits; and private employees always face higher rates of separation and always quit at higher rates than public employees with even the massive separations from the census workers only reduced the difference marginally. Even though the evidence clearly shows that government employees have the lowest turnover rates, we must be cognizant that there may be a selection bias happening here. That is, those that desire jobs that have less turnover would also have the ability to fit into an organization for the long-term. Those that desire long-term job stability would also have traits that allow them to stay on the job long-term.

ConclusionsClearly, government workers stay much longer at their job and have the lowest turnover rates. They feel very content at their jobs and are not leaving or quitting which tells us that the job benefits are of greater value to them than the alternatives. A priori reasoning suggests that the benefit package that government employees get is greater than what the private sector provides. These benefits are beyond just pay checks and benefits but stability of their jobs and overall work and working conditions. It was calculated that this lower turnover rate amounts to around a 12% pay raise. That would be a subjective determination from each individual employee as to the value of this factor along with what individual's discount rate would be. The Heritage Foundation uses utility functions to calculate this additional benefit for increased job security and conclude that it could be as high as 15% of pay for California Public Employees {

Are California Public Employees Overpaid? | The Heritage Foundation}.

However, properly accounting for retiree health benefits and defined-benefit pension plans generates a public compensation premium of around 15 percent. The additional job security granted to public-sector employees is equivalent to an approximately 15 percent increase in public compensation, meaning that the total public-sector pay premium in California may be as high as 30 percent.

Maybe whether they are overpaid or not is immaterial as they are benefiting more than others that are suffering in this economic recession. Governments could be using their monopsonist market powers to extract either higher rates of productivity or lower rates of pay/benefits or both.

If state and local governments are to balance their budgets then pay of public employees must be considered as it consumes about 44% of state and local spending. At some time, productivity of public workers must be considered. Education is the biggest single category of public employees and thus productivity of teachers will have to be addressed also.

Misc. Links:http://www.cato.org/pubs/tbb/tbb-59.pdf

http://www.cato.org/pubs/journal/cj30n1/cj30n1-5.pdf

Job Security DifferencesRecession of 2008 Exposed True Cost of Public Employee Unions | Tad DeHaven | Cato Institute: CommentaryGovernment Sector Unions-Becker - The Becker-Posner BlogMish's Global Economic Trend Analysis: Gallup: U.S. Job Creation At Post-Recession High; What's Next? How Congress Can Spur Job CreationFive Things You Might Not Know About Public Employees presents some facts that important to figuring out how to balance government budgets.

Arnold Kling on Government Wages | RortybombMortality and Lifetime Income: Evidence from U.S. Social Security RecordsQuits (Levels and Rates) - FRED - St. Louis FedTotal Separations (Levels and Rates) - FRED - St. Louis FedWisconsin public versus private employee costs: Why compare apples to oranges? Jeffrey H. Keefe February 15, 2011Unions: Bob Barro's Mistaken Analogy, David Henderson | EconLog | Library of Economics and LibertyWhat’s wrong with ‘right-to-work’: Chamber’s numbers don’t add upDoes ‘right-to-work’ create jobs? Answers from OklahomaMish's Global Economic Trend Analysis: Goldman's Blood-Sucking Leeches Model, Money Multipliers, Macroeconomic Dark Ages, the Taylor Rule, and Nonsense from TrichetMish's Global Economic Trend Analysis: Paul Krugman, Stephen Colbert, Bill Maher, others, Ignore Extortion, Bribery, Coercion, and Slavery; No One Should Own You!Caught: Krugman's Shifting Arguments - Robert P. Murphy - Mises DailyCalculations:How to Calculate Default Risk Ratio | eHow.comA Simplified Method for Calculating the Credit Risk of Lending PortfoliosVolatility Definition - How to Calculate VolatilityHow to Calculate Volatility | eHow.comHow to Calculate Sharpe Ratio | eHow.comLabels: Macro-Economics, Paul Krugman